Occasionally, EAB’s Business Affairs Forum examines topics of interest to a particular segment of our membership—in this case, institutions with academic medical centers. If you have suggestions for focused segments or themes, we welcome your input at [email protected].

30-second summary

30-second summary

- AMC patient care revenue will continue to grow in coming years—but rising costs threaten to wipe out any positive margins.

- Med schools, increasingly reliant on clinical care revenue for their teaching and research expenses, may bear the brunt of these financial challenges.

- Local factors are important in determining whether universities should scale up or create more distance from AMC operations—but an organizational change is not a cure-all.

- Download this AMC-University Relationship Risk Analysis to assess where you’re at now—and where you might need more information or resources.

Last December, Moody’s Investors Service downgraded its financial outlook for the higher education sector in 2018 from stable to negative—and issued similar guidance for the not-for-profit and public healthcare sector. Analysts covering both industries expressed concerns about expenses—concentrated in staff, facilities, and technology investments—outpacing the growth of revenues, whether student tuition or patient care reimbursement.

Academic medical centers (AMCs)—the large, complicated institutions charged with delivering cutting-edge health care, conducting ground-breaking research, and training the next generation of physicians—are likely to feel these pressures most directly. Depending on the financial and organizational ties at play, these AMC margin troubles can exacerbate operational pressures of affiliated universities.

Financial pressures passed to the medical school

In coming years, the top lines of AMCs are expected to continue to outperform other hospitals, largely due to a greater volume of higher acuity and therefore more profitable cases, with a 5-7% growth in patient care revenue forecasted for FY2018 and FY2019. Yet an expected 7-8% increase in patient care expenses among AMCs during the same period threatens to completely erase these margins. Common drivers pushing the revenue and expense lines to cross include:

- Large infrastructure and technology investments to maintain top-tier diagnostic and research capabilities

- Elevated recruiting costs to attract and retain medical specialists

- Low Medicaid, Medicare, and commercial insurance reimbursement rates

- Stagnant or declining levels of federal and state funding for medical research and education

- Cost-control measures introduced by the Affordable Care Act

- Physician time spent on less “profitable” research and education, rather than just clinical care

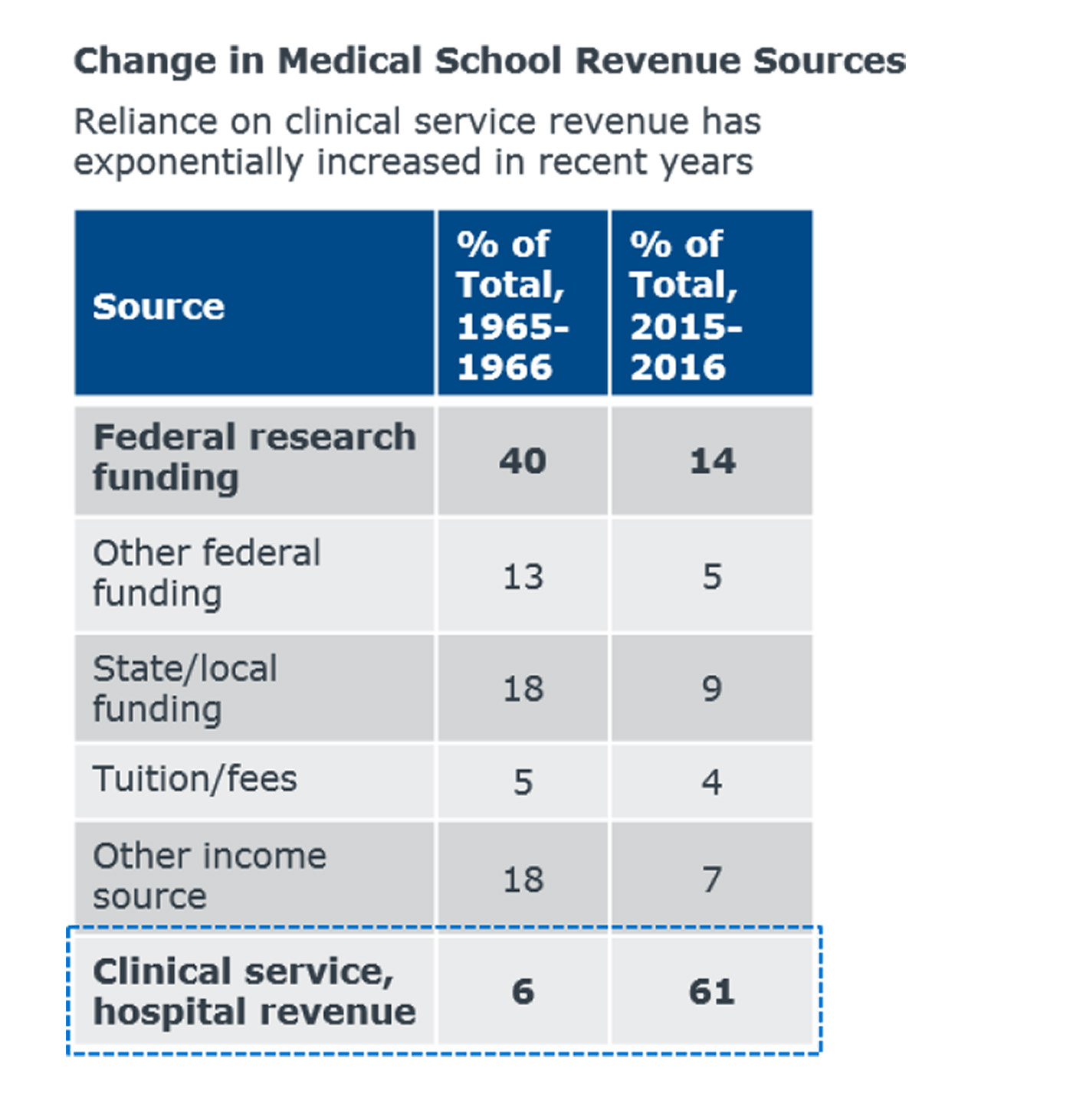

These financial pressures are often passed from the AMC to the affiliated university via the medical school, which relies on clinical service revenue and transfers from the AMC to fund teaching and research operations. In the chart Change in Medical School Revenue Sources, we show a dramatic shift in the primary funding source of medical schools across the last fifty years: away from federal research dollars and toward clinical service revenue. It’s an open question for some institutions whether, at the current course and speed, AMCs will be able to produce enough clinical revenue to subsidize the research and academic mission.

Responding to market pressures via new organizational strategies

In response to market and margin pressures, leaders of some AMCs are turning to organizational solutions. An organizational change will not fix everything, but the underlying benefits are worth noting. Mergers, acquisitions, and partnerships with primary- and secondary-care providers—while complex—can benefit both sides of the deal:

- The AMC sees a strengthened referral stream, extension into local communities, insulation in a competitive environment, and a better position from which to be thinking about primary care, population health, and other risk-based payment models

- The partner institutions receive a boost from the brand of the AMC, access to specialists, expert consultations, and more robust service lines

Alternatively, some universities have created greater organizational and financial distance from their AMCs. Such a change can strengthen the academic institution in three ways:

- First, by relieving the share of leader bandwidth devoted to the health care system for issues more closely related to the core academic mission.

- Second, by alleviating concerns about the growing and outsized share of health care in the university budget, particularly given flattening tuition revenue and enrollment.

- Third, by distancing the university’s financial responsibility for distressed and underperforming health care delivery systems.

Risks—and opportunities—dependent on local conditions

When assessing risk, local conditions–including your organizational structure—will influence your ability to inflect change. Beyond structural considerations, other risks are common to all types of university-AMC relationships. Take the following two steps to capture a snapshot of your current AMC-university risk profile, which can be used to stimulate conversation and analysis with stakeholders:

1. Find your institution on this overview of AMC-university relationship types—and review the questions that your institution should be asking.

2. Walk through this risk analysis diagnostic to analyze your exposure to risks that span all AMC-university relationships.

As the health care market evolves, getting an updated, holistic handle on your AMC’s risk profile can support ongoing ERM processes or provide an opening to refresh your cabinet or board’s engagement with these complex partners.

Citation: Association of American Medical Colleges, AAMC Data Book: Medical Schools and Teaching Hospitals by the Numbers, Washington, DC: AAMC, 2017, 61-65.