The graduate funding shift is here. Are your pricing and aid strategies aligned?

In my seven years guiding graduate institutions on financial aid and pricing strategies, I’ve seen how changes in student financing can quickly show up in enrollment outcomes. As new borrowing limits take effect and Grad PLUS loans are phased out on July 1, many institutions are still underestimating how these shifts will affect student demand, pricing decisions, and net tuition revenue (NTR)—in the near term, and for years to come.

Below is a brief overview of the shifting landscape, along with three steps finance and enrollment leaders can take now to align enrollment and aid strategy, protect your bottom line, and ensure students have the clarity they need to move forward.

The borrowing landscape is changing faster than most aid and enrollment strategies

Cost of attendance is now the single most important factor in students’ graduate enrollment decisions, ranking above reputation, faculty, and career outcomes. Programs that don’t feel affordable are removed from consideration, in some cases regardless of quality.

How will the end of Grad PLUS affect students?

For the last twenty years, Grad PLUS loans have provided graduate and professional students with a streamlined way to finance their education up to the total cost of attendance. But that safety net is going away. While currently enrolled students and those who secure funding before July 1 will be grandfathered into the existing structure, future students will face new borrowing limits, added complexity, and greater financial constraints.

Under the new OBBBA policy, aggregate federal borrowing will be capped at $100,000 for most graduate students ($20,500 annually), and up to $200,000 for professional programs* ($50,000 annually). More than half of graduate borrowers are expected to require additional funding beyond these new limits. At the same time, reliance on external funding continues to grow, with nearly half of students expecting to use loans, grants, or scholarships to finance their education.

*The Education Department has designated 11 degree programs as professional: pharmacy, dentistry, veterinary medicine, chiropractic, law, medicine, optometry, osteopathic medicine, podiatry, theology and clinical psychology.

Students expect—and will need—more financial support to enroll. But as federal financing options narrow and graduate scholarship and aid budgets remain limited, many will face new gaps in funding. Some students may turn to private lenders, but those who choose not to or fail to meet credit approval standards may find themselves with an offer of admission and no way to pay. Institutions that do not respond to this shift risk lower yield and increased late-stage melt.

“We don’t rely on Grad PLUS. How will we be affected?”

Even institutions whose students haven’t historically relied on Grad PLUS loans will feel the impact of these changes. The effects extend beyond borrower eligibility and are compounded by broader market disruptions such as international enrollment trends and the demographic cliff. As borrowing constraints tighten and student price sensitivity increases, the overall pool of prospective graduate students is likely to shrink, intensifying competition.

At the same time, you can expect to see your competitor set shift. Institutions that have relied more heavily on Grad PLUS may respond by adjusting pricing, discounting, or recruitment strategies to address funding gaps and maintain enrollment. These pricing changes will have ripple effects across the market, affecting institutions regardless of their past reliance on federal borrowing.

In this environment, even small shifts in pricing, aid strategy, or perceived value can have an outsized impact on yield, enrollment, and ultimately NTR.

Understand Your Enrollment and Revenue Risk in a Constrained Borrowing Market

Pricing, aid, and enrollment strategy misalignment is a hidden risk

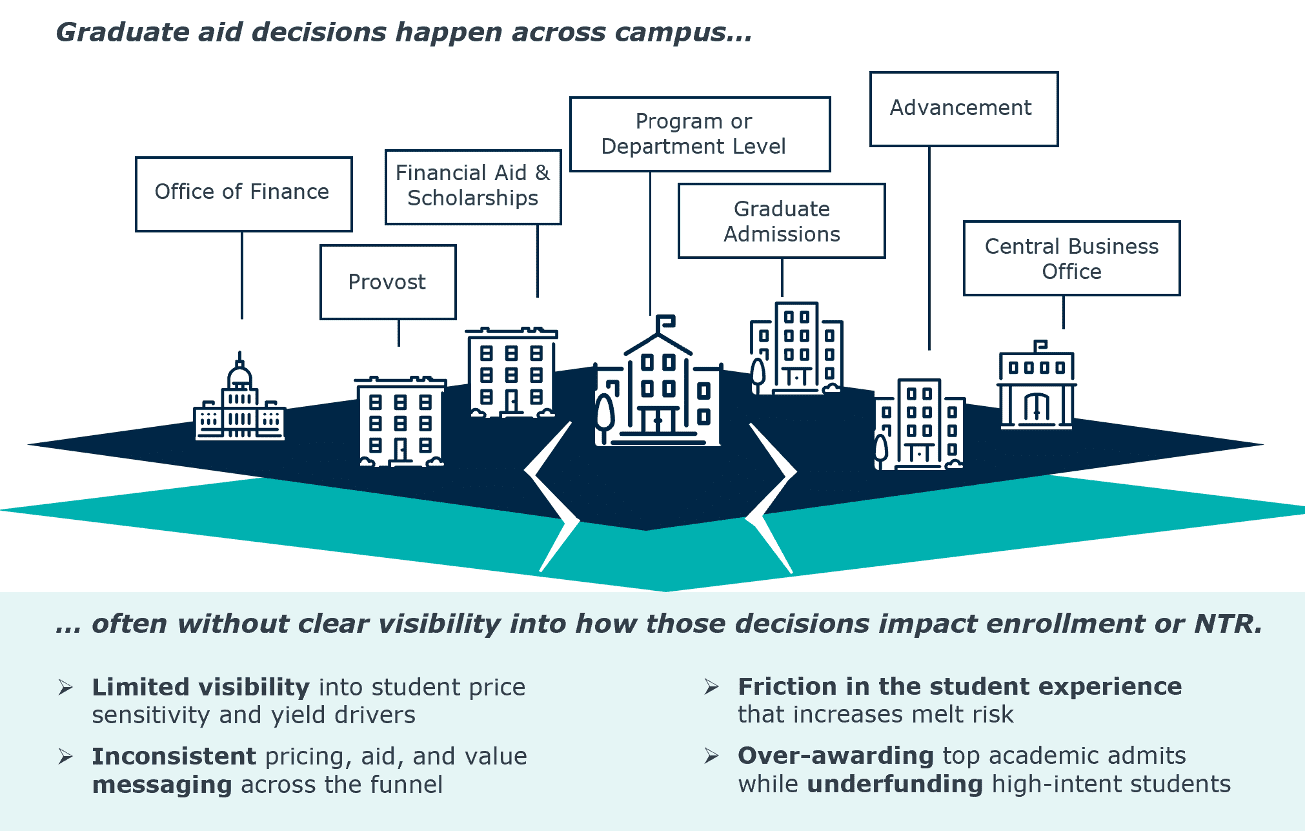

Too often, decisions about program portfolio, enrollment goals, tuition pricing, and financial aid are made in silos rather than as a coordinated effort. These decisions span academic departments, admissions teams, and centralized student financial aid offices, often without a shared view of how they impact enrollment outcomes or NTR.

This lack of coordination shows up in how institutions price programs, allocate aid, and communicate cost to students.

For example, institutions may over-award highly qualified students who were likely to enroll anyway, while underfunding price-sensitive, high-intent students. Pricing decisions may be made without fully considering student price sensitivity or yield behavior and are often driven by internal priorities rather than how students understand cost. As a result, rates and fees can be unclear, making it harder for prospective students to understand what they will actually pay.

A three-part framework for reducing enrollment risk and protecting revenue

To respond effectively to these changes, leaders across graduate enrollment, finance, and aid need a more coordinated and data-driven approach. This framework offers a starting point.

1. De-silo your aid and enrollment strategies

Misaligned, uncoordinated aid and enrollment strategies cause more than confusion for students. Those gaps lead to increased melt, lost prospect interest, and duplicative efforts for staff.

A unified strategy looks like:

- Aid, pricing, and enrollment teams align on program goals and student demand

- Enrollment and marketing teams clearly and consistently communicate cost, aid, financing options, and next steps

- Staff across offices are equipped to guide and hand off students through funding conversations without friction

When enrollment and aid strategies are aligned, students understand both cost and value earlier, and fewer fall out of the funnel due to confusion or uncertainty.

Here’s where you should start:

- Connect leaders from enrollment, marketing, and aid to develop comprehensive and holistic pricing and aid strategies, factoring in historical data and student behavior

- Develop and share a communication plan with relevant staff across offices and provide training to support students at each stage

- Ensure external messaging on cost, scholarships, aid, financing options, and payment plans is accessible and consistent across all communications channels (see more below in part 3)

2. Identify risk and model options

To remain competitive, institutions must move beyond one-size-fits-all funding assumptions. This includes knowing which programs rely most heavily on federal borrowing (usually high-cost programs with limited institutional aid funding), which students are most price-sensitive, and where the greatest risk of melt exists between deposit and enrollment.

Answering these questions requires modeling different pricing and aid scenarios and understanding the trade-offs between headcount and NTR. Institutions that do this well can proactively adjust strategy rather than react to shortfalls.

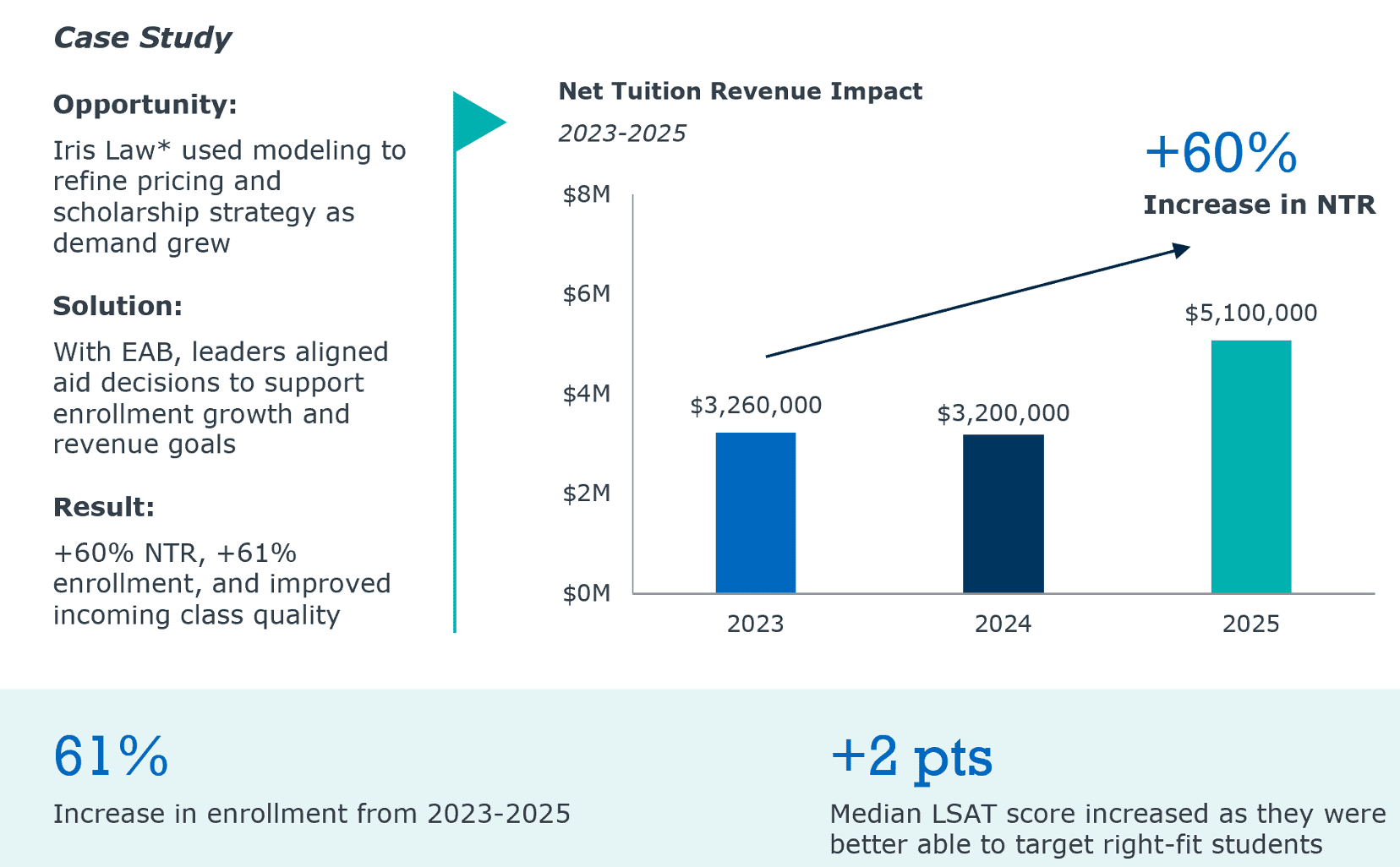

EAB’s Graduate Financial Aid Optimization team helps institutions design data-informed pricing and aid strategies that improve enrollment outcomes, strengthen competitiveness, and protect net tuition revenue. Using advanced modeling and sophisticated data analytics, we help graduate leaders evaluate trade-offs, refine pricing and aid strategy, and make more confident decisions in a changing financial landscape.

Here’s where you should start:

- Assess your current pricing and aid strategy at the institutional and program levels, along with your visibility into scholarship and award practices across campus

- Run a competitive net price and scholarship scan to understand how you compare to peers based on publicly available data

- Model pricing and aid scenarios and test trade-offs before adjusting strategy

3. Communicate cost and value with precision

Clear, coordinated messaging is critical to the student experience. Students expect transparency around total cost, available aid, and return on investment. Share this information with them via marketing emails, your program web pages, and comprehensive FAQs. Institutions must connect price to outcomes such as career pathways, salary potential, and program flexibility early to engage right-fit students.

Just as important, communication must be coordinated at each stage in the funnel. From inquiry through the first day of class, students need timely, relevant information about how to finance their education and what steps to take next. Now more than ever, sustained engagement is critical—a deposit is no longer a guarantee of enrollment.

Here’s where you should start:

- Clearly and prominently display cost of attendance information on your program pages, highlighting available aid and scholarship options

- Connect cost to outcomes (e.g., career, salary, and advancement opportunities)

- Highlight speed to completion and program flexibility

The urgency is real and the window to act is narrow

Policy changes take effect July 1, but their impact will be felt for years to come. In today’s borrowing-constrained market, the institutions best positioned to navigate this shift are those that take a proactive, data-informed approach to how they set price and allocate aid.

That means identifying where you’re most exposed and modeling how different pricing and aid strategies will influence enrollment and NTR. Most importantly, pricing, aid, and enrollment strategies must work together rather than at odds.

The cost of inaction goes beyond declining enrollment. It includes missed opportunities to engage right-fit students, inefficient use of aid dollars, and increased revenue uncertainty.

Ready to learn more?

If you’re looking to better understand your risk exposure or evaluate your current strategy, our team of financial aid experts can help.

More Blogs

6 trends we're watching after the end of Grad PLUS

How to improve graduate student retention